Sticking to a financial plan is crucial for achieving long-term financial success. It provides a roadmap for reaching your financial goals and helps you stay on track, even when faced with unexpected expenses or market fluctuations. However, many people struggle to stay committed to their financial goals. Whether it’s due to lack of discipline, unexpected expenses, or simply losing motivation, it can be challenging to stick to a financial plan. In this article, we will discuss the importance of sticking to a financial plan and the challenges people face in doing so. We will also outline some strategies for staying committed to your financial goals, including creating a realistic budget, setting achievable milestones, and regularly reviewing and adjusting your plan as needed.

Understand Your Financial Goals

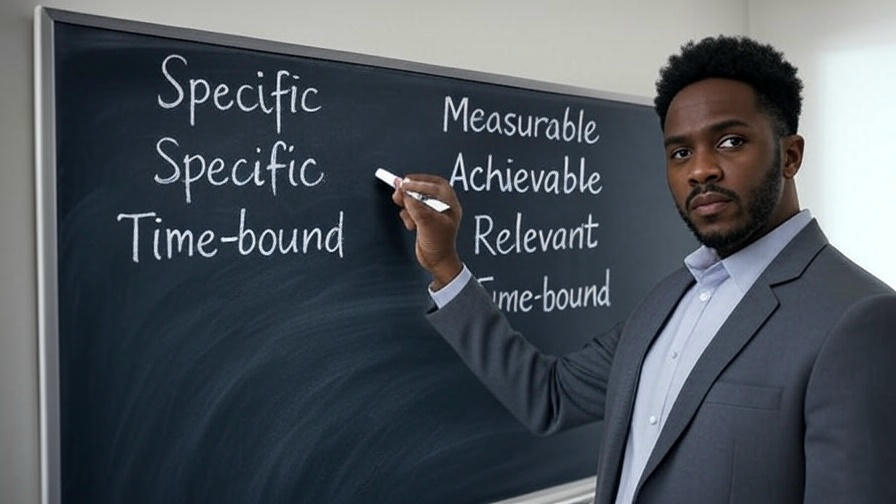

It is essential to clearly define short-term, mid-term, and long-term financial goals in order to create a strategic and effective financial plan. By using the SMART goal framework – making goals Specific, Measurable, Achievable, Relevant, and Time-bound – individuals can set clear and attainable targets for their financial future. Understanding the importance of different time frames for financial goals helps individuals prioritize their saving and investment strategies. Short-term goals may include saving for a down payment on a house or paying off high-interest debt. Mid-term goals might involve saving for a child’s education or a major home renovation. Long-term goals could include retirement savings or building wealth for future generations.

Create a Realistic and Flexible Budget

Step 1:

Track your income – Start by calculating your monthly income from all sources, including your job, side hustles, and any other sources of income.

Step 2:

Categorize expenses – List all your monthly expenses and categorize them into fixed expenses (such as rent, utilities, and loan payments) and variable expenses (such as groceries, entertainment, and dining out).

Step 3:

Set saving targets – Determine how much you want to save each month and allocate that amount in your budget. This will help you prioritize saving and ensure that you are working towards your financial goals.

Automate Your Finances

Automation can help prevent impulse spending by setting up automatic transfers from your checking account to a savings account or investment account. By having a portion of your paycheck automatically deposited into these accounts, you can ensure consistent saving without the temptation to spend that money impulsively. Additionally, setting up automatic bill payments for monthly expenses can help you avoid late fees and ensure that you are consistently saving money for future goals. By taking advantage of automation, you can develop healthy financial habits and achieve your saving goals more effectively.

Setting up automatic transfers to savings, retirement accounts, and investment portfolios is a smart financial move. By automating your savings, you can ensure that you consistently contribute to these accounts without having to remember to do so each month. This can help you build up your savings and investments over time and make progress towards your long-term financial goals. It’s a convenient way to prioritize your financial future and make sure you are consistently putting money towards your savings and retirement.

Build an Emergency Fund

An emergency fund is crucial for achieving financial security and staying on track with your financial plan. It provides a safety net for unexpected expenses such as medical emergencies, job loss, or major car repairs. Without an emergency fund, you may be forced to rely on high-interest credit cards or loans, which can derail your financial goals. Financial experts recommend saving 3-6 months’ worth of living expenses in an emergency fund. This amount allows you to cover essential costs while you get back on your feet in the event of a financial setback. It’s important to assess your individual situation and consider factors such as your income stability, family size, and potential expenses to determine the ideal amount for your emergency fund.

Regularly Review and Adjust Your Plan

Tracking progress toward goals is important because it allows you to see how far you’ve come and stay motivated to continue working towards your objectives. It also helps you identify any areas where you may need to adjust your plan to stay on track. When circumstances change, such as a change in income or unexpected life events, it’s important to be flexible and adjust your financial plan accordingly. This may involve re-evaluating your goals, reworking your budget, or finding new ways to save or earn money. Reviewing your financial plan quarterly or annually is essential to ensure that it still aligns with your current financial situation and goals. This allows you to make any necessary adjustments and stay on track towards achieving your objectives.

Control Your Spending Habits

Identifying and eliminating unnecessary expenses is an important step in achieving financial stability. One technique for mindful spending is the 30-day rule, which involves waiting 30 days before making a non-essential purchase to determine if it’s truly necessary. Distinguishing between needs and wants can also help prioritize spending on essential items. Setting limits for discretionary spending without feeling deprived can be achieved by creating a budget and allocating a specific amount for non-essential purchases. This allows for guilt-free spending within set boundaries. Building habits of intentional saving and investing involves making regular contributions to a savings account or investment portfolio. This can be achieved by automating savings and investing, making it easier to build a financial cushion for the future.

Stay Accountable

Accountability partners play a crucial role in helping you stick to your financial plan. You can choose from a variety of options, such as a financial advisor, family members, support groups, or even apps that track your progress. These individuals or tools can provide support, guidance, and motivation to help you stay on track. When facing setbacks or experiencing slow progress, it’s important to stay motivated. One way to do this is by celebrating milestones and rewarding yourself for sticking to your plan. This can help you stay focused on your long-term goals and remind you of the progress you’ve made. Remember that setbacks are a normal part of the process, and it’s important to stay positive and keep pushing forward.

Educate Yourself About Personal Finance

Financial literacy is incredibly important in making informed decisions about your money. There are a variety of resources available to help you improve your financial knowledge. Books such as “Rich Dad Poor Dad” by Robert Kiyosaki and “The Total Money Makeover” by Dave Ramsey offer valuable insights into personal finance and investing. Online courses like those offered by Khan Academy and Coursera can provide structured and comprehensive education on topics ranging from budgeting to retirement planning. Podcasts like “The Dave Ramsey Show” and “The Tim Ferriss Show” feature interviews and discussions about financial topics, while blogs like “The Penny Hoarder” and “Mr. Money Mustache” offer practical tips and advice.

Conclusion

In the article, we covered several strategies for overcoming financial challenges and maintaining long-term financial discipline. Some of the key points included setting specific financial goals, creating a budget and sticking to it, building an emergency fund, avoiding debt, and investing for the future. As you move forward, it’s important to take actionable steps today to secure a better financial future. This might include tracking your spending, finding ways to increase your income, and staying focused on your long-term goals. I encourage you to start creating your financial plan today for lasting success. By taking control of your finances and making a commitment to long-term financial discipline, you can achieve greater stability and security in the future.