Did you know that nearly 40% of Americans don’t have enough savings to cover a $400 emergency? It’s crucial to start saving money, especially for beginners, in order to build a secure financial future. In this article, we will cover a step-by-step guide for beginners on how to start saving and build wealth. We will discuss the importance of saving, practical tips for saving money, and how to set achievable financial goals. Whether you’re just starting out or looking to improve your financial habits, this article will provide valuable insights to help you on your journey to financial stability.

Understanding the Basics of Saving

What does it mean to save?

Saving in the context of personal finance refers to setting aside a portion of income for future use rather than spending it immediately. This can be done through various methods such as putting money into a savings account, investing in stocks or bonds, or contributing to a retirement fund. Savings are important for several reasons. Firstly, they provide financial stability by creating a safety net for unexpected expenses or emergencies, such as medical bills or car repairs. Additionally, savings can help individuals work towards future goals, such as buying a house, starting a business, or retiring comfortably. By saving consistently, individuals can also take advantage of compounding interest and grow their wealth over time.

The difference between saving and investing:

Saving and investing are both important components of financial planning, but they serve different purposes. Saving is a safer and more liquid form of money management, typically done through a savings account or certificate of deposit. It allows you to set aside money for short-term goals or emergencies, and it offers easy access to your funds. On the other hand, investing involves taking on more risk in pursuit of potential higher returns. It typically involves putting money into stocks, bonds, mutual funds, or other assets with the goal of growing your wealth over the long term. While investing has the potential for greater returns, it also comes with the risk of losing money.

Assessing Your Financial Situation

Tracking income and expenses:

It is important to track your income and expenses in order to have a clear understanding of where your money is going. This helps you make informed decisions about your finances and allows you to identify areas where you can potentially save or cut back on expenses. Budgeting is a key component of managing your finances and it involves creating a plan for how you will allocate your income towards various expenses and savings goals. By tracking your income and expenses, you can better adhere to your budget and ensure that you are meeting your financial goals. For beginners looking to track their spending, there are a variety of tools and apps available that can help simplify the process.

Understanding debt:

Debt can have a significant impact on your ability to save. High-interest debt, such as credit card debt, can eat away at your income and leave you with less to put towards savings. Addressing and paying off high-interest debt should be a priority before saving more aggressively. By tackling your debt first, you can free up more of your income to put towards savings in the long run. It’s important to make a plan to pay off your debt as efficiently as possible in order to improve your financial situation and start building a solid savings foundation.

Setting Clear Savings Goals

The importance of having specific savings goals:

Setting specific savings goals is important because it provides direction and motivation for saving. When you have a clear goal in mind, such as saving for a down payment on a house or a vacation, it gives you a target to work towards. This can help you stay focused and disciplined in your saving habits. Additionally, having specific savings goals can also help you prioritize your spending and make informed financial decisions. For example, if you know you are saving for a specific goal, you may be less likely to make impulse purchases or overspend on non-essential items. When it comes to saving, it’s also important to differentiate between short-term and long-term goals.

SMART goals for savings:

SMART goals are a great way to set achievable and meaningful savings targets. The acronym stands for Specific, Measurable, Achievable, Relevant, and Time-bound. This means that your goals should be clear and well-defined, easy to track progress on, realistic, important to you, and have a specific deadline. For beginners, some realistic examples of SMART savings goals could include saving for a vacation, creating an emergency fund, or saving for a down payment on a house. For example, a SMART goal for saving for a vacation could be to save $1,000 in 6 months by setting aside $167 per month.

The Best Savings Strategies for Beginners

Start with a budget:

Creating a budget with a savings category is a great way to take control of your finances and start building up your savings. One popular budgeting method is the 50/30/20 rule, which allocates 50% of your income to needs, 30% to wants, and 20% to savings. To make saving easier, consider automating your savings. Set up automatic transfers from your checking account to your savings account on a regular basis. This way, you can save without even having to think about it. Another helpful tip is to set up automatic deposits on your payday. This way, a portion of your paycheck goes directly into your savings account before you even have a chance to spend it.

Pay yourself first:

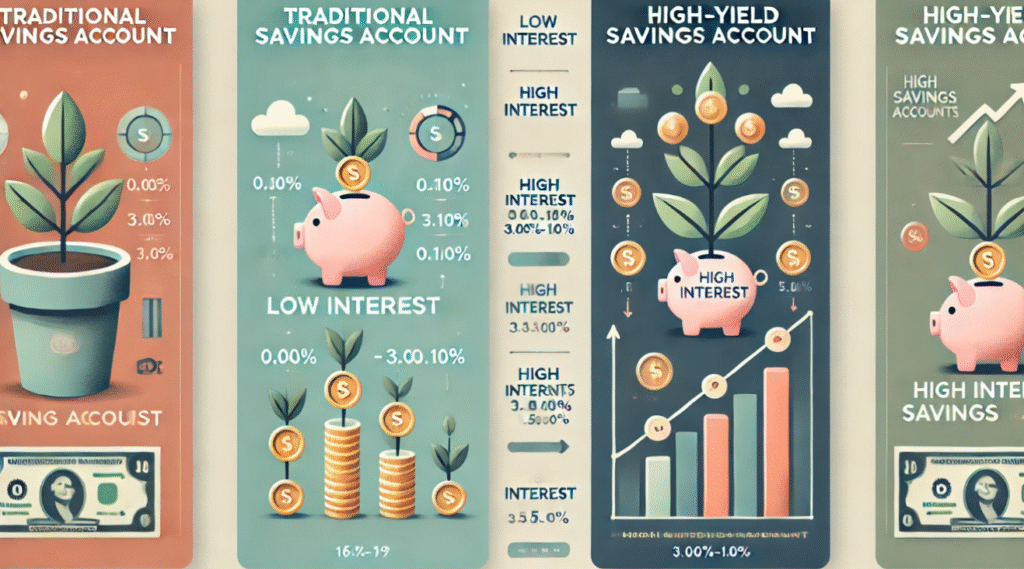

Paying yourself first is a concept that involves allocating a portion of your income towards savings before spending on discretionary items. This ensures that you prioritize your financial well-being and future goals. High-yield savings accounts offer higher interest rates compared to traditional savings accounts, allowing your savings to grow more quickly over time. Some reputable online banks or credit unions that offer high-yield savings accounts include Ally Bank, Marcus by Goldman Sachs, and Discover Bank. Building an emergency fund is crucial for financial stability, as it provides a safety net in case of unexpected expenses or loss of income. Experts recommend having 3-6 months of living expenses saved in an easily accessible account.

Overcoming Common Saving Challenges

Overcoming the temptation to spend:

Saving money in a world filled with consumerism and impulse buys can be quite challenging. With advertisements bombarding us from all angles and the constant pressure to keep up with the latest trends, it can be difficult to resist the temptation to spend. One effective strategy for controlling spending urges is to implement the 24-hour rule for major purchases. This involves waiting a full day before making a significant purchase, which allows time for reflection and helps to avoid making impulsive decisions. When it comes to dealing with unexpected expenses, it’s important to recognize that life is full of surprises and having an emergency fund in place can help mitigate the impact of these unforeseen costs.

Staying motivated:

Staying motivated to reach savings goals can be challenging, but there are several strategies that can help you stay focused. One effective approach is to set specific milestones along the way to your ultimate savings target. Breaking your goal into smaller, more manageable steps can make it feel more achievable and keep you motivated. Additionally, rewarding yourself for reaching these milestones, even in small ways, can help to maintain your momentum. Whether it’s treating yourself to a small indulgence or simply acknowledging your progress, these rewards can serve as positive reinforcement for your efforts. By implementing these tactics, you can stay motivated and on track to reach your savings goals.

Leveraging Compound Interest and Other Savings Options

What is compound interest?

Compound interest is a powerful concept in finance that allows your savings to grow exponentially over time. Unlike simple interest, where you earn interest only on the initial amount of money deposited, compound interest allows you to earn interest on both the initial principal and the accumulated interest. This means that your money grows at an increasing rate, accelerating your savings over time. For long-term goals like retirement, compound interest can make a significant difference in the amount of money you have saved. By regularly contributing to an investment account, you can take advantage of the power of compound interest to grow your savings over many years. The longer your money is allowed to compound, the greater the impact it will have on your overall savings.

Savings options for beginners:

For beginners looking to start saving, there are several options to consider. Certificates of Deposit (CDs) are a low-risk option that offer a guaranteed return over a set period of time. Employer-sponsored 401(k) plans are another great option, especially if your employer offers a matching contribution. Individual Retirement Accounts (IRAs) are also a popular choice, offering tax advantages and a variety of investment options. As you become more comfortable with saving and are ready to start investing, consider index funds or mutual funds. These options offer diversification and professional management, making them a great choice for beginners looking to grow their savings over the long term.

Conclusion

In the article, we covered several key savings strategies for beginners. These included setting specific savings goals, creating a budget, tracking expenses, automating savings, and taking advantage of employer-sponsored retirement plans. I encourage you to start implementing these strategies now and make savings a priority in your financial planning. By starting early and being consistent with your savings efforts, you can build a strong financial foundation for the future. I encourage you to take the first step today, whether it’s setting up a savings account, tracking your expenses, or automating your savings. The sooner you start, the sooner you’ll see the impact of your efforts.